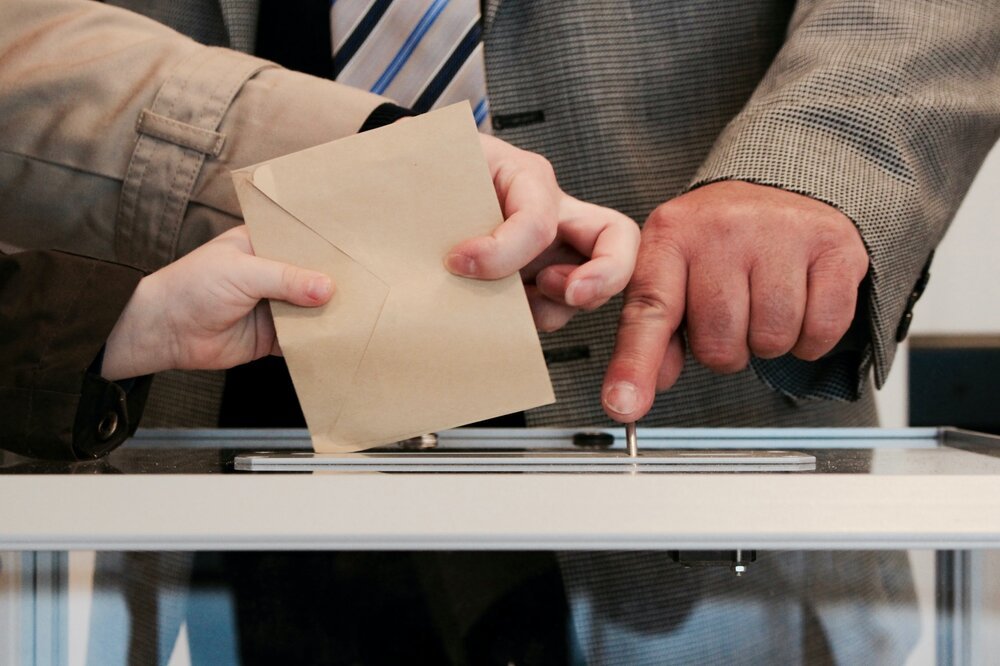

Policy preview: referanda to the rescue?

Planning reform has long been seen as a bugbear for the Conservative Party. Even the current government, with its 80-seat majority, has faced calls to water-down its proposals in the aftermath of June’s Chesham & Amersham by-election attenuated concerns that housing reform could erode support from the traditional Conservative base, homeowners.

The Labour Party has attempted to seize on this, arguing that Prime Minister Boris Johnson’s tax increase puts the burden to fund social care on workers rather than on homeowners. Nonetheless, we noted in our 23 June Horizons newsletter that we expected Johnson to push ahead with the core of these reforms despite that shock result with the Liberal Democrats overturning a 16,000 majority.

Johnson and Housing Secretary Robert Jenrick, however, have faced grumbling from the backbenches, including from former prime minister Theresa May over the planning reforms. Yet some of these same backbenchers may have picked up on a solution that allows Johnson to avoid risking a major rebellion. MPs are expected to introduce a private members bill that would give local communities a vote on housing in their area, including approving density plans and style guides.

The policy, known as ‘Street Votes,’ is the brainchild of the Policy Exchange and Create Streets think tanks and aims to challenge the perception that new developments are aesthetically, and economically, unpleasing to suburban residents while also enabling those rural residents to protect green spaces even when their local authorities aim to increase the housing stock.

Whether such a policy could be successful remains to be seen. Advocates such as Sam Bowman of the US’ International Center for Law and Economics argue that it provides the optionality necessary to have a ‘bottom-up’ approach while allowing the political hurdles, at both a parliamentary and local level, to be overcome by residents keen on raising the value of their neighbourhood. They point to similar proposals in Seoul and Tel Aviv that saw new housing approvals jump by as much as 50%.

Incorporating the Street Votes proposals into the government’s own legislation may well bring it sufficient votes to avoid a substantial rebellion. It may also bring in some Labour votes for Johnson’s housing plans and planning reforms, a situation Johnson has thus far been keen to avoid least he be seen to be dependent on Labour votes to pass them.

The Smart Votes system remains untested, and it will seem unnatural to many UK political observers that referenda, even of the hyper-localised variety, could be the panacea to some of its mot lasting political disputes. Politically, however, it offers the Johnson government the potential to declare victory on passing its reforms while deflecting responsibility for any eventual housing -target shortfall.

“Maybe this referendum will be the beginning of a trend” Former UKIP and Brexit Party leader Nigel Farage

Power play: waiting for Whately

The UK government is staking a great deal of political capital on its recently announced reforms for adult social care. Prime Minister Boris Johnson has gripped the ‘third rail of British politics’ by trying to tackle the issue, but the government could be damaged if the controversial policy is a damp squib.

Helen Whately, Minister for Social Care, will be responsible for driving and delivering the reforms. Funded by a rise in national insurance contributions and dividend taxes raising £12bn annually, the government will initially attempt to clear the pandemic-induced NHS backlog.

After three years of increased funding for the NHS, the extra cash will supposedly be diverted from the NHS and re-allocated to the social care system. If, of course, reducing funds to the NHS doesn’t prove too politically challenging.

With a political bid to prevent care users needing to sell their homes or other financial assets to fund their social care, the government has proposed a (means-tested) cap on the lifetime costs of social care of £86,000 from October 2023.

However, it is not yet clear exactly how or why the reforms will make the social care system. The political difficulty that has surrounded the issue for decades has largely been a matter of funding, and it is this area that was covered in most detail by last week’s announcement

There is still more to come in the way of solutions for how the government plans to tackle some of the underlying problems that the social care sector faces. Identified in Department for Health & Social Care’s white paper this February, these issues include insufficient integration with the NHS, too much bureaucracy and a need for more accountability in the system.

The government’s new plan includes provisions for more training and support for care workers, but detail on how it will address these issues is thin on the ground, with another white paper setting out further detail promised in due course. Social care providers such as Four Seasons Health Care have already criticised the plan as being too little too late, calling on the government to make the necessary reforms to help support staff as soon as possible.

Though the reforms have not been universally popular, they have not torpedoed the Conservative’s polling in the manner that Theresa May’s social care proposals did in 2017. Once the impact of NIC increase starts to bite, pressure will be on for the government and for Whately to show that their reforms are having a real effect.

“We have a social care crisis right now, and it can’t wait to for people to draft [a promised white paper], and then delay any funding and any staffing changes for another two years.”

Jeremy Richardson, Four Seasons Health Care CEO

Dollars and sense: actioning ESG

It is not too often that international bond markets have to think about NGO’s. That is not to say it is unprecedented for them to do so – 25 years ago the International Monetary Fund and World Bank launched the Highly Indebted Poor Countries (HIPC) initiative following sustained pressure from the Jubilee Debt campaign and associated activist groups. HIPC today remains a key structure of emerging market debt markets, enabling many more countries, including debuts well into the bottom rungs of the credit rating spectrum, to issue international debt.

The sale of so much debt by low-income countries and companies in poorly regulated markets has often raised concerns about how they should be treated for investors seeking to put climate change concerns and environmental, social and governance (ESG) principles at the heart of their investing strategy. The credit investment industry is being slowly transformed by ESG investing, with so-called ‘green bonds’ now often trading at a premium. This makes green debt in theory cheaper, and therefore a market structure to promote the very ESG principles they encompass.

However, concerns about ‘greenwashing’ remain. If the recent trend for ESG investing does translate to a sustained premium, this risks major losses for creditors holding debts that are later revealed not to be as rooted in ESG as initially premised.

Given that similar concerns about morality in investing and the potential for economic growth to be more equitable globally prompted the HIPC initiative – which enables countries below a certain income level to receive special assistance from the IMF and World Bank – it is not too surprising that once again the voices of NGO’s are being heard on ESG investing.

Already there is evidence that they may be having an impact. In March of this year, the Nature Conservancy announced it was launching a programme to work with coastal nations to protect their waters, ‘Blue Bonds for Ocean Conservation’. The effort attempts to combine the twin realities that it is difficult for maritime nations to resist exploiting their waters’ wealth with the reality that debt countenancing ESG principles is cheaper for issuers.

The Nature Conservancy said that it was inspired to launch the programme by work it had done with the Seychelles government to restructure $22 million in its debts in 2016, but it is now set to face its first major market test. The government of Belize has announced its intent to restructure its debt – following two defaults in recent years – in a deal backed by the Nature Conservancy and its key creditors. Under the Blue Bonds programme, Belize will repurchase $530 million in dollar bonds for just over US$290 million. Investors see a gain to the 60% discount the debts had been trading at, while Belize reduces its debt burden substantially. In exchange it agreed to fund a $23.4 marine preservation endowment and the new debt provided by Credit Suisse to finance the repurchase will be subject to Belize continuing to honour certain ESG commitments. The deal has until 19 November to be approved by 75% of bondholders.

Bringing together international institutions, NGOs and bond markets proved an effective way to fund emerging markets growth with the HIPC initiative. The Nature Conservancy programme may just have established a template for ensuring that ESG principles remain a sustained, not fleeting, feature of funding this growth.

“A debt is just the preservation of a promise” David Graeber, Author of Debt: The First 5,000 Years